{kind=link}

You are less than 60 seconds away from your quote.

Resume from where you left off. No obligations.

Refinancing your mortgage during Chapter 13 can provide a means of achieving financial stability and a pathway to a fresh start.

NOTE: There may be additional eligibility requirements depending on the details of your Chapter 13 bankruptcy. At the bottom of this page, we’ve outlined the requirements for various loan products for Chapter 7, Chapter 11, and Chapter 13 bankruptcy.

TEXAS RESIDENTS: Only private money solutions are available, requiring at least 40% equity and interest rates above 10%.

Chapter 13 bankruptcy, often referred to as a wage earner’s plan, allows individuals with a “regular income” to develop a plan to repay all or part of their debts. Chapter 13 bankruptcy involves a repayment plan over three to five years. This type of bankruptcy shows your commitment to repaying your debts and can be viewed more favorably by lenders when considering refinancing options.

Refinancing during a Chapter 13 bankruptcy can present unique challenges, but it also offers potential benefits. It may allow you to take advantage of lower interest rates, reduce your monthly mortgage payment, or consolidate your debts into one manageable payment. However, qualifying for refinancing during Chapter 13 bankruptcy involves meeting stricter criteria than a standard refinance. Lenders will want to see evidence of your commitment to financial stability, including proof that you’ve made consistent payments on your bankruptcy plan for at least a year, among other requirements.

Navigating through a Chapter 13 bankruptcy can be daunting, and when you have an existing mortgage to refinance, the journey might seem even more challenging. However, at JVM Lending, we are committed to providing you with the necessary tools and expertise to help you find a path through this process. Let’s explore how refinancing your mortgage during a Chapter 13 bankruptcy can be possible and beneficial.

Refinancing during a Chapter 13 bankruptcy can yield numerous benefits:

Everyone’s situation is unique. Connect with a JVM Lending mortgage expert to see how a refinance could benefit you and discuss your refinancing goals.

Here are the key criteria you need to meet to refinance during Chapter 13 bankruptcy:

NOTE: There may be additional eligibility requirements depending on the details of your Chapter 13 bankruptcy. At the bottom of this page, we’ve outlined the requirements for various loan products for Chapter 7, Chapter 11, and Chapter 13 bankruptcy.

Interest rates will play a key role in assessing the viability of your refinance while you are in a Chapter 13 bankruptcy. Your Chapter 13 filing will likely have adversely impacted your credit score, which could result in a higher interest rate than you would otherwise be offered if your filing had not impacted your score. The good news is that FHA mortgages tend to have lower interest rates in general than other types of mortgages such as conforming (Fannie Mae) mortgages. In addition, the impact to your rate from a lower credit score may not be significant, depending on how low your score is. If your credit score is above 640, for example, the impact will be minimal, and if it is above 659, there will be no impact.

If rates have dropped since you took out your original mortgage, you could actually lower your interest rate and payment while refinancing within your bankruptcy.

One of the most attractive benefits of refinancing during Chapter 13 bankruptcy is the ability to consolidate your debts. By leveraging the equity in your home, you can do a cash-out refinance to pay off some or all of your existing debts. This can provide immediate relief during a Chapter 13 bankruptcy and even take you out of your bankruptcy altogether – accelerating your path toward financial stability.

We are experts at debt consolidation refinancing and love helping our clients save on their monthly debt payments. Get in touch with us or call (855) 855-4491 to see how we might be able to help you.

Understanding the refinancing process during a Chapter 13 bankruptcy can help you navigate it more smoothly. Here are the key steps involved:

1) Ensure You Are Meeting Requirements

Before you can lock in your interest rate, you need to satisfy certain debt-to-income ratio (DTI) and property equity criteria. This involves providing income documents, like paystubs and W2s, and determining your property’s value.

2) Home Appraisal

An appraisal will be ordered to formally confirm the value of your home and the amount of equity you have.

3) Approval and Closing

Once your appraisal is complete, your underwriting approval is in hand, and your court sign-off is secured, your refinance will be ready to close. Keep in mind that court approval can sometimes take several weeks, depending on the volume of cases.

Below is a breakdown of the steps where your lender will directly help with:

After successfully refinancing during a Chapter 13 bankruptcy, there are still a few considerations to keep in mind:

Credit Impact

The impact to your credit from your bankruptcy is likely substantial, and the impact will remain for some time. It will, however, diminish quickly if you are able to pay off some or all of your debts via a refinance. We encourage borrowers to rebuild their credit as quickly as possible in order to restore their good standing.

Financial Management

Refinancing can be a significant step towards regaining financial stability, but it should be paired with responsible financial management. This includes creating a realistic budget, keeping up with your payments, and avoiding new debts that could jeopardize your financial recovery.

Long-term Planning

The goal of refinancing during bankruptcy is to put you on a path towards long-term financial stability. This involves not just managing your current financial situation, but also planning for your future financial needs.

Remember, navigating through a Chapter 13 bankruptcy and the refinancing process can be challenging, but you don’t have to do it alone. At JVM Lending, our team of experts is ready to guide you through every step of the way.

If you have read this far, you know that the answer is yes. Please, however, review the eligibility criteria above.

Yes, but it might affect the interest rate you receive. If, however, your credit score is still above 580 and you meet all of the other qualifying criteria, you should have no trouble refinancing.

FHA loans require that you have lived in the property as your primary residence for at least 12 months. For an FHA loan, you can refinance your loan balance up to 96.5% of the property’s value on a rate and term refinance.

Refinancing involves one-time closing costs such title insurance, escrow fees, appraisal fees, notary fees, and loan processing fees. These costs can, however, potentially be rolled into your new loan amount or covered by a lender credit – so they should not be intimidating if your cash position is tight. Please also note that the closing costs associated with a bankruptcy refinance are usually not higher than they would be for a standard refinance. There are also “recurring closing costs” such as mortgage interest and homeowner’s insurance, but these are costs that you would have to pay whether you refinance or not; they are just mentioned here as a reminder that you will have to front some of these recurring costs as part of your overall closing costs should you refinance. And, if you have sufficient equity, recurring closing costs can also be rolled into your loan.

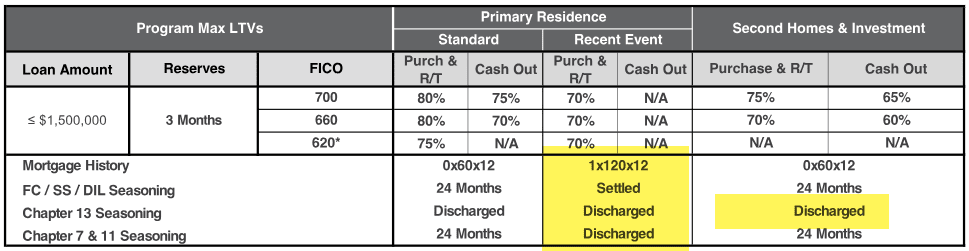

NOTE: Borrowers with a discharged Chapter 13 Bankruptcy are subject to the same rules as Chapter 7 & 11 filers, so it is often better for Chapter 13 filers to apply for a mortgage BEFORE their bankruptcy is discharged.

NOTE: Borrowers with a discharged Chapter 13 Bankruptcy are subject to the same rules as Chapter 7 & 11 filers, so it is often better for Chapter 13 filers to apply for a mortgage BEFORE their bankruptcy is discharged.

NOTE: Review this matrix and contact JVM Lending for additional explanation

NOTE: Hard money or private money loans are loans that do not require any income or credit documentation at all, as they focus solely on equity – with the exception of compensating factors.**

NOTE: These mortgages have high interest rates and are short-term in nature. They should only be obtained if there is no other alternative and there is a clear plan to re-establish credit within one to two years when a refinance into a much better mortgage will be a viable option. These mortgages are, however, also excellent vehicles to be used in the short-term to re-establish credit, when sufficient equity is available. We have many hard money sources at JVM and are happy to match them to your needs.

At JVM Lending, we have a highly experienced team that specializes in diverse mortgage loan products, including Chapter 13 bankruptcy refinance loans. We are committed to offering competitive rates while ensuring a personalized service experience for each of our clients. We are equipped with the knowledge and skills to guide you through the complexities of the loan process and will be your trusted partner throughout your homeownership journey.

Our team at JVM Lending is here to guide you every step of the way. Start your JVM loan application online or contact us today at (855) 855-4491 to discuss your refinance goals.

CONTACT

Guaranteed 60-minute responses during operating hours

Resume from where you left off. No obligations.