You are less than 60 seconds away from your quote.

Resume from where you left off. No obligations.

Real low rates. Real people. Real easy.

Get your custom rate quote with:

based on 1,180 reviews

homebuying tools you need

Our no-loan-officer model gives us a leg up against other mortgage lenders.

How this benefits youBuy A Home

JVM's Famous Fast 14

Our 14 calendar day close increases the odds of getting your offer accepted and lets you get into your new home at record speed.

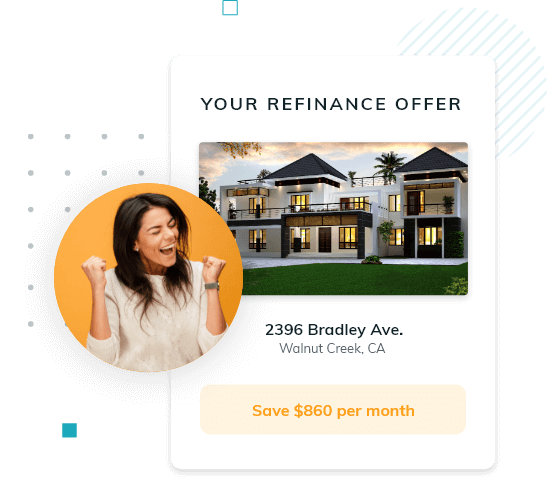

Refinance Your Home

Low Rates

We have low rates for every loan type. Our best rates are posted daily here.

We'd be happy to take a look to see if we can match it or offer you better terms.

Use our Rate Comparison Tool to help you analyze all your options.

Seize low rates instantly with JVM Rate Watch© alerts! Slash loan costs and maximize savings. Don't wait – join now!

We ensure our rates are always among the lowest in the industry and ~ 0.25% LOWER than the national average.

Learn moreOur superior technology and highly advanced systems provide the best and most seamless client experience in the industry.

Learn moreOur super team of highly trained mortgage experts is available 7 days a week to answer all of your questions.

Learn moreOur team of experts is not on commission, so you will never be pressured or pushed to do anything you don’t want to do.

Learn moreJVM Lending definitely came to our rescue. After having a bad experience with another lender, our agent Mariama connected my wife and I with JVM Lending. They immediately turned our situation around in such short notice, or best said, the same day. They were able to lock our interest rate at such reasonable rate. Wesley and Kelsey were such amazing people to work with. They made the process a million times easier. They were there in every step of the entire paper work and answered every single question we had. My wife and I are now HOMEOWNERS thanks to the amazing JVM team! If you are looking for a professional, responsive and incredible lender, JVM is your go to.

Rigo D.

JVM, where do I begin? Oh, I know! They are the best team that make it very seamless for agents and clients. I began using them in recent months when I moved teams and let's say I wish I found out about them much sooner. Working with Aaron and Victor, these two are the dream team. Whenever I had questions or my clients had questions not only where they both fast to respond but they rolled out the red carpet and provided a 5-star limo service ride. My clients were able to get their offer accepted in this competitive market with a fast 15 days close all thanks to Aaron and Victor. SO GO WITH JVM OR BE STUCK HOUSE HUNTING FOR A LONNNNNNNG TIME!

Jorge R.

My husband and I were first-time homebuyers and JVM made what is such a scary and unknown thing so easy! We decided to go with JVM as a recommendation from my little brother (1st-time home-buyer too) and my mother (relocated to the bay area from NOLA), who both had amazing experiences with JVM. Boy, are we happy we made that decision, JVM exceeded all our expectations! We closed on our home in Concord in 21 days. They answer questions and emails within hours, sometimes within minutes. They truly went above and beyond to make sure we had everything we needed to make decisions, navigate all the paperwork and the technology is so user-friendly. They have really thought of everything to make this experience a pleasure!

Erika B

Being a first time home buyer, I was certainly overwhelmed by the many steps necessary to take when buying a home. Luckily a close friend referred us to JVM as the excellent choice for first time home buyers. And she was right! Not only is JVM very well known and established in the Bay Area but their team was very professional, knowledgeable, quick to respond, and always willing to answer questions - and I had many! I highly recommend JVM to anyone looking for a lender who will really work with you and explain things thoroughly. They are thorough with their due diligence (and it makes sense why) but once you're past this step, you're really in good hands. Thanks again JVM for your help and for giving us the opportunity to buy our first home. We couldn't be any happier!

Angel J.

The team at JVM was fantastic to work with. We worked with Victor, Larisa, and Jennifer on the different stages of the process and they were all extremely knowledgeable and helpful every step of the way. The online portal was also very easy to use. We were able to close even earlier than expected due to the excellent communication and great service provided by the team. I would highly recommend JVM to all my family and friends.

Ben F.

I went through JVM for my home mortgage, and everyone that I have dealt with has been incredibly knowledgeable and helpful. I am very grateful to have gone through them for this experience. I have to give a special thanks to Emily Albertson, who has gone above and beyond for anything that I have gone to her for. Even after the fact, her follow up and responsiveness has been unmistakable from a professional who truly cares about other people. Thank you so much for all that you have helped me with Emily!

S. T.

Writing this as a Realtor that has worked with JVM over many clients! I only have great things to say... the team at JVM thoroughly educates buyers, is quick to respond to calls and emails, they do pre-underwritten preapprovals which local agents know is gold... but moreover, their reputation precedes them. Agents know how solid that JVM pre-underwritten approval is, and it definitely helps me do my job better for my clients. Overall, during the entire course of helping a buyer buy a home, they help me to help my clients better. Love having JVM Lending as part of my team! They are seriously Lender Ninjas!

Tanja O.

I first learned about JVM Lending through my inner circle. I was extremely impressed with how fast the process was and also that JVM Lending gave me a competitive interest rate. Natalie Nolan, Hannah Papazian, and Paige Berglund were so nice and they communicated very quickly. I felt that JVM Lending took me seriously as a first-time homeowner and went out of their way to ensure that all of my questions were answered. I have shared with my coworkers and social network how exceptional JVM Lending is and I will continue to refer people that I know to this wonderful organization!

Astrid H.

We could not have been more satisfied with JVM Lending. The service, attentiveness, and communication we received was unmatched, and they went above and beyond to answer all our questions and work WITH us throughout the entire home-buying and closing process. Thank you, Wesley and team for your outstanding support!!

Deme P.

We chose JVM after speaking with several different lenders. As first-time homebuyers, we appreciated that JVM was quick to respond to questions and went into great detail while explaining each step of the lending process. Even our realtor commented that she was impressed by JVM! The entire team was a pleasure to work with.

Katie B.

JVM Lending gave me a best in class lending experience! They were efficient, responsive, courteous, and lighting fast. I was able to close my mortgage loan in just over two weeks. And because there is such an emphasis on employee cross-training and putting the customer first, the service is excellent. Many thanks to the staff, especially Nik and Connie!

Farhana C.

This is my second time working with JVM. My first experience was so wonderful and easy that when it came time to sell my house and buy another one, there was no question who I should reach out to. And the second time was just as pleasant as the first. Wesley and Jess were both very communicative, understanding, accommodating, and knowledgeable. We had a particularly odd situation with our transactions and they helped navigate us through each potential hurdle. They helped us land our dream home, but if we are ever in need again, JVM will be my first call.

Tyler G.

We match you to the loan and interest rate that will make your home your best investment yet.

We are committed to reinventing the mortgage lending model in order to provide outstanding service, low rates, and some of the fastest closing times in the industry.

Resume from where you left off. No obligations.