TEXAS DISASTER CERTIFICATIONS

This is a brief notice to all of our Texas clients that many lenders are now requiring a Disaster Certificate before they will fund a loan. This usually entails another interior inspection by an appraiser – to certify that properties are free of storm-related damage on a Form 1004D.

PRE-QUAL vs. PRE-APPROVAL

We have touted our JVM Lending Certified® Pre-Approvals for over a decade now, and we are delighted to say that they are now more sought after than ever.

Full pre-approvals, however, require many hours of effort, as we go through every document with a fine-toothed comb to make sure no issues arise once borrowers are in contract (we want to make sure our pre-approvals are deemed “as good as cash” at all times). More complex jumbo loan pre-approvals may require multiple third-party verifications from employers and landlords, which can add even more time to the process.

Our problem is this: B/c of our success and b/c of the hot housing market, we will sometimes get far more requests for pre-approvals than we have manpower to pre-approve in a single day.

This is b/c our pre-approval team not only has to do all of that pre-approval work, they also need to cater to our hundreds of other previously pre-approved borrowers who are coming back for updated letters, questions, new scenarios, requests to call agents, and much more.

TWO CATEGORIES OF BUYERS: OFFERING NOW & JUST LOOKING

In order to provide better service for agents and borrowers alike, we are delineating our borrowers into two categories: (1) Offering Now; and (2) Just Looking.

We will still happily do full pre-approvals for clients who want to make offers now, as we know that no offer will be accepted with anything less than an airtight pre-approval in this market.

For clients with longer buying time-frames, however, we are offering Pre-Qualification Letters that are based primarily on the client’s data input and a credit pull.

These Pre-Qualification Letters serve two purposes for clients: (1) they give clients a sense of what they qualify for right away; and (2) they provide clients with a letter they can use to view houses in a matter of hours.

This is in contrast to our full pre-approvals, which can take several days to complete on occasion if and when the queue gets long.

I want to make it clear though that as soon as any of our “pre-qualified” borrowers want to make offers and have provided all necessary documentation, we will readily and quickly convert their pre-qualification to a complete pre-approval.

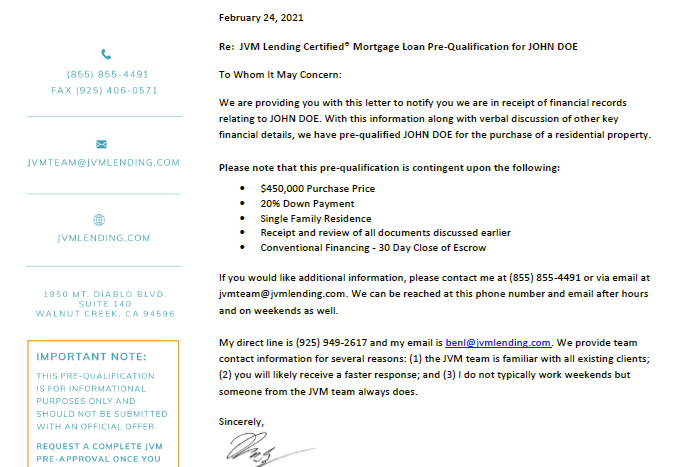

And finally – this is what our Pre-Qualification Letter looks like:

Jay Voorhees

Founder/Broker | JVM Lending

(855) 855-4491 | DRE# 1197176, NMLS# 310167